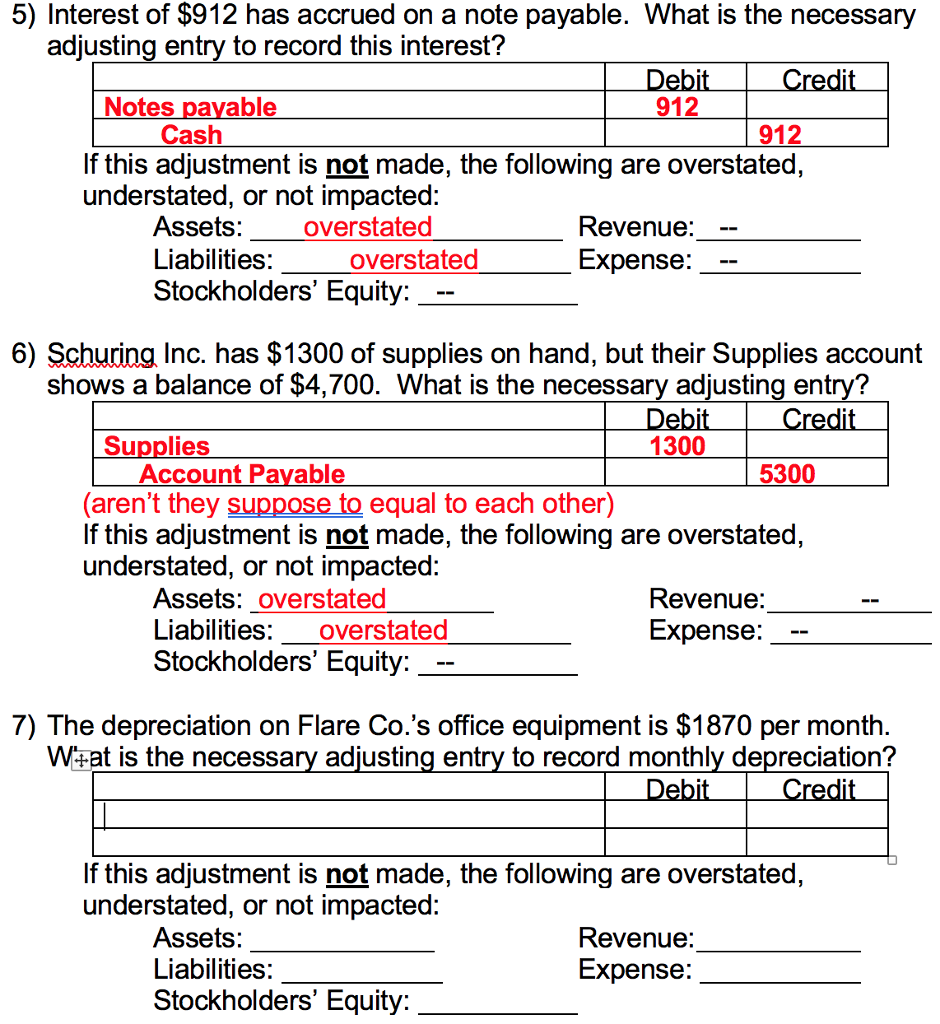

A short-term notes payable created by a purchase typically occurs when a payment to a supplier does not occur within the established time frame. The supplier might require a new agreement that converts the overdue accounts payable into a short-term note payable (see Figure 12.13), with interest added. This gives the company more time to make good on outstanding debt and gives the supplier an incentive for delaying payment. Also, the creation of the note payable creates a stronger legal position for the owner of the note, since the note is a negotiable legal instrument that can be more easily enforced in court actions. As you repay the loan, you’ll record notes payable as a debit journal entry, while crediting the cash account. But you must also work out the interest percentage after making a payment, recording this figure in the interest expense and interest payable accounts.

Stay up to date on the latest accounting tips and training

At some point or another, you may turn to a lender to borrow funds and need to eventually repay them. Learn all about notes payable in accounting and recording notes payable in your business’s books. Short-term debt may be preferred over long-term debt when the entity does not want to devote resources to pay interest over an extended period of time.

How much will you need each month during retirement?

- Cash decreases (a credit) for the principal amount plus interest due.

- When you take out a loan, it’s important to manage your payments carefully.

- Unlike cash-basis accounting, accrual accounting suggests recording a transaction in financial records once it occurs, regardless of when cash is paid or received.

- If you have ever taken out a payday loan, you may haveexperienced a situation where your living expenses temporarilyexceeded your assets.

- There is an ebb and flow to business that can sometimes produce this same situation, where business expenses temporarily exceed revenues.

F. Giant must pay the entire principal and, in the first case, the accrued interest. In both cases, the final month’s interest expense, $50, is recognized. Interest expense is not debited because interest is a function of time. The discount simply represents the total potential interest expense to be incurred if the note remains’ unpaid for the full 120 days.

Note Payable Example Journal Entry

Hence, without properly account for such accrued interest, the company’s expense may be understated while its total asset may be overstated. Of cause, if the note payable does not pass the cut off period or the amount of interest is insignificant, the company can just record the interest expense extension of time to file your tax return when it makes the interest payment. The goal is to fully cover all expenses until revenues aredistributed from the state. However, revenues distributed fluctuatedue to changes in collection expectations, and schools may not beable to cover their expenditures in the current period.

This treatment ensures that the interest element is accounted for separately from the cost of the asset. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping. He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University.

Accounting for Interest Payable: Definition, Journal Entries, Example, and More

A short-term note payable is a debt created and due within a company’s operating period (less than a year). A short-term note is classified as a current liability because it is wholly honored within a company’s operating period. This payable account would appear on the balance sheet under Current Liabilities. A short-term note payable is a debt created anddue within a company’s operating period (less than a year). A short-term note is classified as acurrent liability because it is wholly honored within a company’soperating period. This payable account would appear on the balancesheet under Current Liabilities.

N/P is an additional credit source for businesses aside from accounts payable. It can delay payments for purchases or loans, which gives businesses more flexibility in managing their working capital. However, it has interest charges, which are an additional expense for the borrower. We hope this article helped you understand how N/P is created and how interest affects the amount you pay the lender. They are also considered short-term liabilities if they have maturities of less than 12 months.

All of our content is based on objective analysis, and the opinions are our own. The note in Case 2 is drawn for $5,200, but the interest element is not stated separately. This is because such an entry would overstate the acquisition cost of the equipment and subsequent depreciation charges and understate subsequent interest expense. The present value technique can be used to determine that this implied interest rate is 12%. Therefore, in reality, there is an implied interest rate in this transaction because Ng will be paying $18,735 over the next 3 years for what it could have purchased immediately for $15,000.

This means that the $1,000 discount should be recorded as interest expense by debiting Interest Expense and crediting Discount on Note Payable. In this way, the $10,000 paid at maturity (credit to Cash) will be entirely offset with a $10,000 reduction in the Note Payable account (debit). In the preceding entries, notice that interest for three months was accrued at December 31, representing accumulated interest that must be paid at maturity on March 31, 20X9. On March 31, another three months of interest was charged to expense. The cash payment included $400 for interest, half relating to the amount previously accrued in 20X8 and half relating to 20X9.